Gold vs Oil: The Commodity War Beneath the Geopolitical War

Every geopolitical conflict triggers two markets.

One prices physical disruption.

The other prices loss of trust.

Oil captures the first.

Gold captures the second.

When conflict expands, oil surges because supply chains fracture. Tankers reroute. Insurance premiums explode. Strategic reserves suddenly matter again. Gold rises for a different reason. It signals something deeper: the market’s confidence in the financial system is eroding.

Right now both forces are building at the same time. Middle East escalation, fractured alliances, weaponized trade, and rising fiscal stress are pushing both commodities higher.

The real question for investors is not whether they rise.

It is which one wins the race. Because that answer reveals the next macro regime.

The First Reaction: Oil Always Moves First

Energy markets are structurally fragile.

Nearly 20% of global oil trade flows through the Strait of Hormuz, a narrow corridor that connects Gulf producers to the global economy. When that corridor becomes politically unstable, oil markets reprice risk immediately.

The recent Middle East escalation triggered exactly that reaction.

Brent surged close to $120 per barrel, a near 25% jump in a single trading session. Traders quickly began discussing scenarios closer to $140–$150, levels not seen since the 2008 commodity supercycle.

Oil shocks ripple through the economy with unusual speed.

The IMF estimates that every sustained 10% rise in oil prices adds roughly 40 basis points to global inflation. That transmission forces central banks to keep policy tight even when growth is slowing.

Oil spikes therefore carry a second-order consequence. They turn into monetary policy events.

Gold Is Pricing Something Different

Oil reflects disruption.

Gold reflects distrust.

Historically gold rallies when three macro forces converge:

• geopolitical instability

• declining real interest rates

• central bank reserve diversification

All three are now visible.

The data behind that view is structural. Central banks have purchased more than 3,000 tonnes of gold since 2022, the fastest accumulation in modern reserve history. At the same time, global public debt has crossed $315 trillion, roughly 330% of global GDP, limiting how aggressively central banks can keep real rates elevated if growth slows.

Reserve managers are increasingly wary of a system where currency reserves can be frozen, sanctioned, or politically weaponized. That shift helps explain why gold has already pushed above $5,000 per ounce, a level that few strategists considered plausible just three years ago.

Unlike oil, gold does not require a supply shock.Its price moves when global portfolios reallocate.

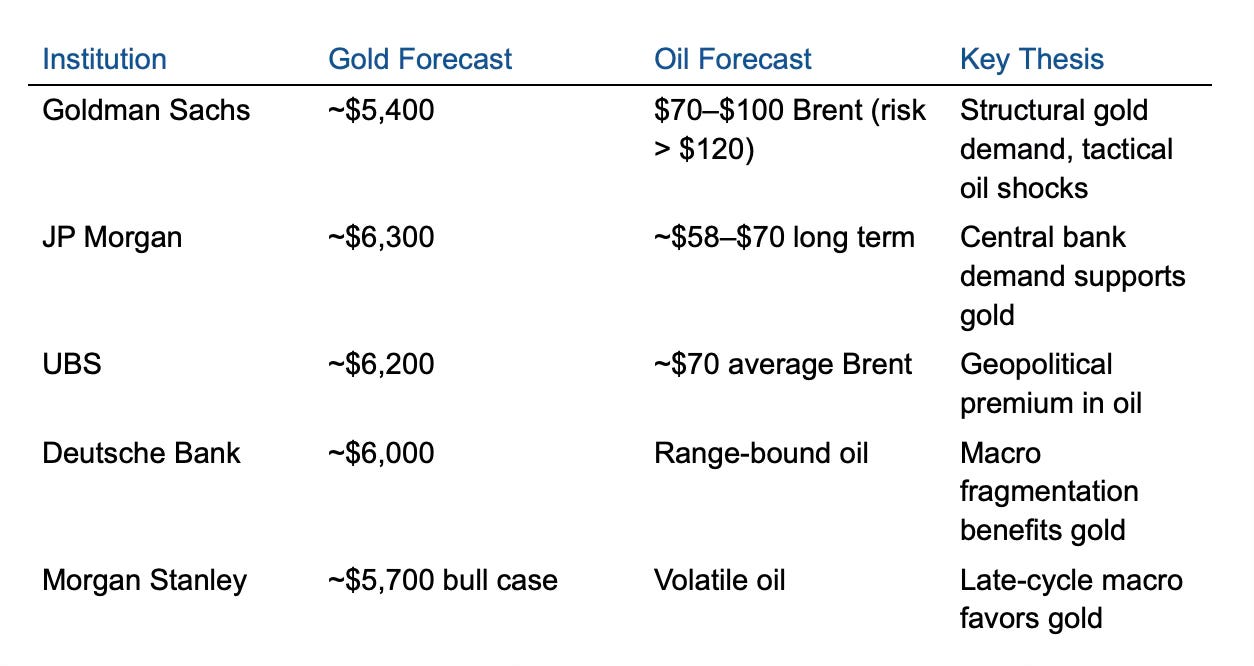

What the Banks Are Saying

Institutional forecasts reveal an important asymmetry.

Oil expectations remain tactical.

Gold expectations look structural.

Institutional Commodity Forecasts (2026)

Across desks, the message is consistent.

Oil shocks come and go.

Gold rallies tend to reprice the system itself.

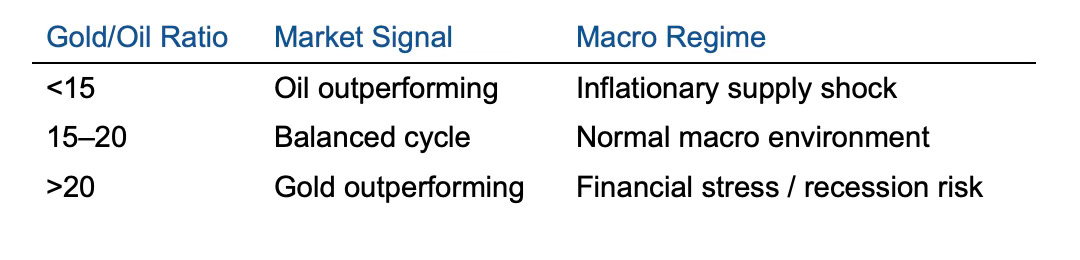

The Indicator Macro Investors Actually Watch

Serious macro investors rarely analyze oil and gold separately. They watch the Gold/Oil Ratio.

Gold/Oil Ratio = Gold Price ÷ Oil Price

The ratio measures how many barrels of oil one ounce of gold can purchase. Over long periods the ratio averages 15–20. It functions as a surprisingly powerful macro signal.

During the 2008 financial crisis, oil collapsed while gold held firm. The ratio surged.

During the 2022 energy shock, oil surged faster than gold. The ratio compressed.

In other words, the ratio answers a deeper question. Is the world facing an energy crisis or a confidence crisis?

Two Macro Paths From Here

The next phase of the cycle determines the winner.

Scenario 1: Energy Shock Dominates

If geopolitical conflict materially disrupts supply:

• Brent crude could move toward $120–$150

• global inflation reaccelerates

• central banks remain restrictive

In this regime, oil outperforms gold.

Scenario 2: Energy Shock Breaks Growth

If high energy prices suppress global demand:

• economic growth slows

• real rates eventually fall

• capital rotates into safe assets

In that regime, gold outperforms oil.

Historically commodity cycles follow a familiar sequence.

Oil spikes first.

Gold rallies later.

The Structural Shift Most Investors Are Missing

The most important change in this cycle is central bank behaviour. For decades central banks were passive participants in gold markets. That era is ending.

Reserve managers are increasingly accumulating gold as insurance against:

• Geopolitical fragmentation

• Sanctions risk

• Fiscal expansion

• Declining confidence in reserve currencies

This shift matters because it transforms gold from a cyclical hedge into a strategic reserve asset. That is a different demand curve entirely.

The Real Signal

The signal from commodity markets is increasingly pointing in one direction: gold is likely to outperform oil over the next phase of the cycle.

The data behind that view is structural. Central banks have purchased more than 3,000 tonnes of gold since 2022, the fastest accumulation in modern reserve history. At the same time, global public debt has crossed $315 trillion, roughly 330% of global GDP, limiting how aggressively central banks can keep real rates elevated if growth slows.

Energy markets, by contrast, are entering a more cyclical phase. Outside of geopolitical disruptions, global oil supply capacity continues to expand through US shale, Guyana, and Brazil, while demand growth is slowing as China’s industrial cycle matures. The IEA expects global oil demand growth to fall below 1 mb/d later this decade, roughly half the pace seen in the early 2010s.

That asymmetry matters. Oil spikes are typically sharp but temporary. Gold rallies tend to persist when they coincide with debt expansion, geopolitical fragmentation, and reserve diversification.

If those forces continue to build, the gold–oil ratio is likely to rise over the coming years. In practical terms, that would signal a macro regime defined less by energy scarcity and more by growing skepticism toward the stability of the global financial system