India Manufacturing Is the Hottest Theme for Investors And Yet the Capital Is Splitting Three Ways

Nearly $2 billion has been pledged to deep-tech and strategic manufacturing alone, yet the sector is still stuck at 16% of GDP.

India manufacturing has become one of the most crowded ideas in finance. In the past two years alone, India-focused private equity fundraising has surged, venture investors have set up a $1 billion deep-tech alliance around strategic manufacturing, and policy support has funnelled incentives into sectors from electronics to semiconductors. Yet the macro scoreboard still looks underwhelming: manufacturing remains stuck at roughly 16% to 17% of GDP, far below the 25% target that has anchored the “Make in India” narrative for years.

So what exactly is all this capital chasing?

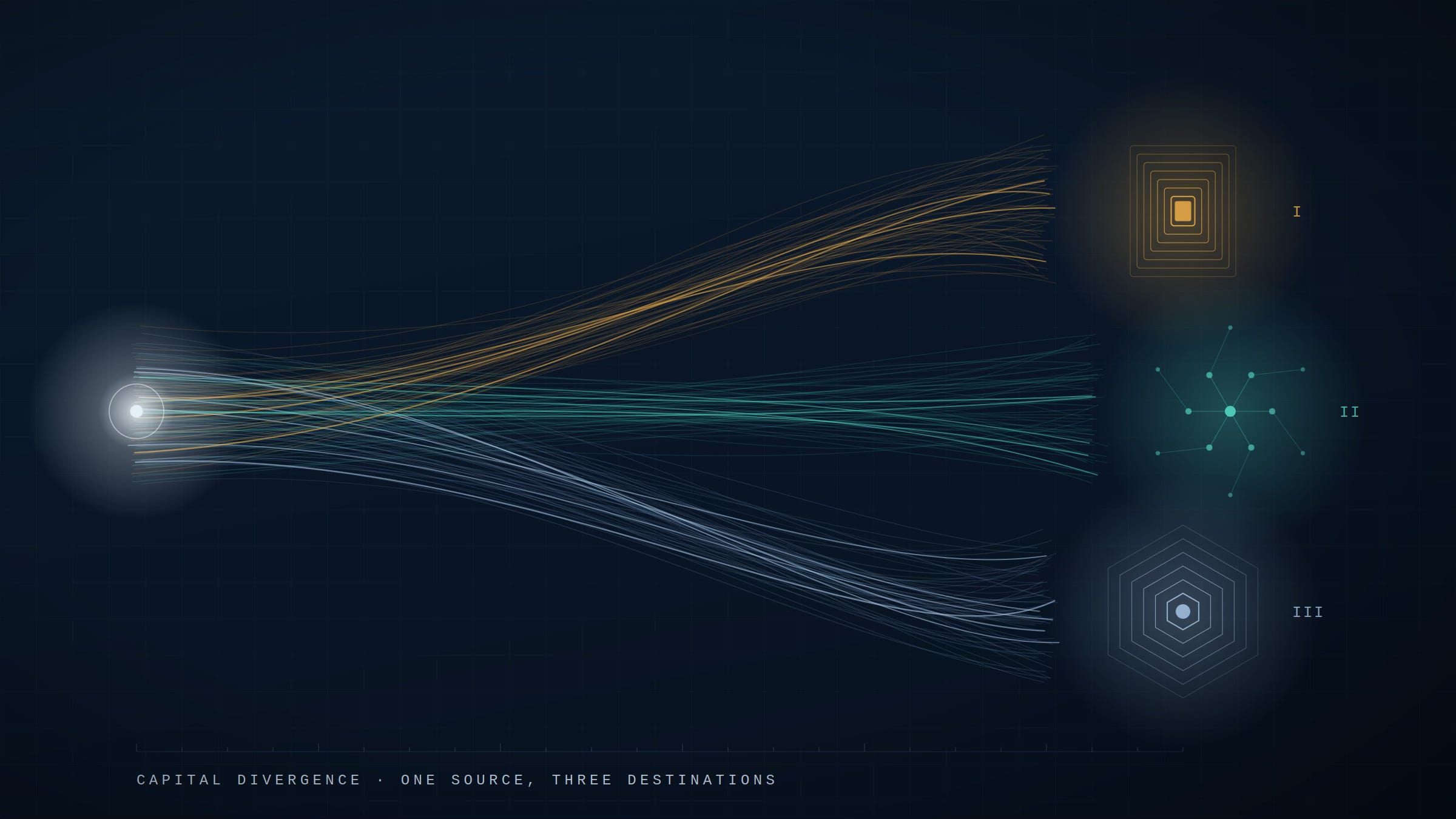

That is the interesting part of the story. The money pouring into “India manufacturing” is not converging on one view of the sector. It is splintering across very different bets on where value will actually sit.

At the macro level, the common pitch is familiar by now: India has domestic demand, rising infrastructure spending, digital rails and a supply-chain tailwind as companies diversify beyond China. JPMorgan’s framing of “India for India” and “India for the world” captures the dual opportunity neatly. But that only explains why capital is interested. It does not explain how investors expect to make money. Once you get beneath the slogan, “India manufacturing” breaks into three distinct investment games.

Private equity: manufacturing as value migration

For private equity and growth investors, manufacturing is not a moonshot or a nation-building story. It is a value-migration story inside already-proven businesses. Bain’s India Private Equity Report 2025 shows how serious that capital has become: Kedaara closed a $1.7 billion fund in 2024, ChrysCapital raised $2.1 billion in 2025, and buyouts accounted for 51% of India PE deal value in 2024, up from 37% in 2022. That is a control-oriented market looking for operational leverage, not just passive exposure to the macro.

What PE is really underwriting is a move up the manufacturing value chain. The target is not a company doing low-margin assembly, but one that can shift into components, formulation, design, export manufacturing or deeper supplier control. That is why sponsor interest has clustered around pharma CDMOs, specialty chemicals, auto components and electronics manufacturing services.

What PE is looking for

Export-oriented, less regulated sectors where sponsors are comfortable taking control and scaling globally, not just riding domestic volume growth.

Value migration rather than pure capacity addition: assembly to components, components to design, or process manufacturing to higher-value formulations.

Pharma CDMOs and specialty manufacturing where customer stickiness, qualification cycles and regulatory complexity create better margins than plain commodity production. Bain notes healthcare deal volumes rose about 80% in 2024, helped in part by CDMO activity.

Auto components and EMS with engineering content, especially EV-linked suppliers or electronics manufacturers trying to move beyond assembly into sub-systems and design.

Backward integration and working-capital discipline. This is particularly important in EMS, where growth can look spectacular but margins remain thin and receivables and inventory can quickly absorb cash.

Founder willingness to institutionalise. In Indian mid-market manufacturing, a large part of PE value creation still comes from professionalising reporting, procurement, capital allocation and governance.

The best way to think about the PE manufacturing trade is simple: sponsors are not buying factories for the sake of it. They are buying businesses that can capture a larger share of the manufacturing economics without getting trapped in commodity assembly.

Venture capital: manufacturing as IP and strategic hardware

Venture capital is playing a different game altogether. Here, manufacturing is less about cash flow and more about intellectual property, strategic capability and long-duration technology bets. The clearest signal came in September 2025, when Accel, Blume, Celesta, Premji Invest and others launched the India Deep Tech Investment Alliance with a pledge of more than $1 billion over a decade, later joined by Nvidia as a technical adviser and Qualcomm Ventures as an investor. That was not just a funding announcement. It was an acknowledgement that deep-tech manufacturing needs a different capital model from software.

In this bucket, “manufacturing” means semiconductors, defence and space systems, drones, robotics, batteries and advanced materials. The factory matters, but the real asset being funded is IP: design capability, technical know-how, proprietary hardware and eventually strategic export relevance.

What VC is looking for

Manufacturing categories where the product is really IP-heavy hardware: semis, drones, defence systems, robotics, batteries and industrial deep tech.

Build-for-India, then export models, especially in defence and aerospace, where India’s operating conditions and procurement needs can serve as a proving ground.

Long-duration platforms that can justify seven-to-twelve-year development cycles, rather than software-style growth expectations.

Policy-supported sectors where state funding, procurement or RDI support improves the odds of patient capital being rewarded.

A software or recurring-revenue layer on top of hardware. This is the maturing nuance in the market. Even hardware investors increasingly want autonomy software, analytics or data services layered over the physical product to avoid purely lumpy procurement economics.

The venture version of manufacturing, then, is not really a factory story. It is a strategic-technology story being expressed through hardware.

The third trade: manufacturing without owning the factory

The third group of investors agrees with the macro thesis but wants none of the factory risk. Their bet is on the enabling layer: the supply-chain, procurement, software and contract-manufacturing networks that sit on top of India’s fragmented industrial base. Zetwerk is the clearest example. Its value proposition is not owning one giant manufacturing asset, but using software and network orchestration to connect customers with a broad supplier base across categories and geographies.

This is a very different way to play the same trend. Instead of underwriting plant utilisation, capex cycles and factory-level execution, these investors are underwriting fragmentation. The opportunity is to make India’s manufacturing base easier to source from, monitor, finance and scale.

What this capital is looking for

Platforms that aggregate fragmented manufacturing capacity rather than owning all of it.

Supply-chain orchestration and procurement software that reduce friction for customers and create repeat usage.

Capital-light exposure to China+1 and export diversification, without taking direct plant risk.

Embedded control points such as vendor management, quality assurance, fulfilment, logistics or working-capital support.

The appeal is obvious. If India’s manufacturing buildout continues, some of the most attractive economics may sit not in the factory itself, but in the layer that coordinates hundreds of factories more efficiently.

The common filter: avoid “screwdriver assembly”

Despite their different time horizons, these investor groups are screening for the same thing: value addition. The single sharpest distinction in India manufacturing today is between businesses that merely assemble imported inputs and businesses that control a more valuable part of the chain.

Across PE, VC and the enabling layer, the recurring filters are strikingly similar:

Value-add over assembly: investors want businesses moving from assembly into components, design, formulations, process know-how or proprietary hardware.

Backward integration: control over key inputs, modules or upstream processes remains one of the clearest signs that margins can improve.

Export capability: the strongest manufacturing stories increasingly use India as a base for global customers, not just local volume.

Working-capital discipline: especially in EMS and industrial supply chains, topline growth can hide poor cash conversion.

Governance and professionalisation: still a major source of value creation in founder-led Indian manufacturing businesses.

This is the real dividing line between fundable manufacturing and hype. Investors are not paying up for capacity alone. They are paying for the chance to escape commodity economics.

The skeptic’s case

The skeptics still have a case. Manufacturing remains stuck at roughly 16% to 17% of GDP, well below the 25% aspiration that has framed “Make in India” for years. India is still far from China’s scale as a manufacturing power, and while the PLI scheme and China+1 have clearly boosted sectors such as electronics, pharmaceuticals and auto components, the gains have not yet translated into a broad-based jump in manufacturing’s share of the economy.

That is exactly why granularity matters. The investors most likely to make money from India’s manufacturing push are not underwriting the macro slogan. They are underwriting specific parts of the value chain where economics improve faster than the aggregate data does. Private equity is buying margin migration in proven industrial businesses. Venture capital is backing IP-heavy hardware and strategic manufacturing. And a third group is betting that the best way to monetise the trend is to own the software and supply-chain layer wrapped around it.

India manufacturing may be one of the hottest themes in finance. But the capital flowing into it is already telling a more precise story than the slogan suggests.